Financial Mis-selling Terms & Conditions

Terms of Engagement

- What is it that Direct Redress Limited will do for you?

- We will assess your claim and if appropriate, pursue a claim for the recovery of your losses, on your behalf.

- We will deal with all aspects of your claim, including all correspondence. This includes all negotiations where required with relevant companies and/or institutions.

- On occasion, it may be necessary for us to obtain further information from you including signed documentation to make this possible.

- We will, if needed, pursue your claim with the Financial Services Compensation Scheme, the Financial Ombudsman Service (or other regulatory body) at no additional cost to you.

- We will inform you of all and any offers of settlement that we receive, evaluate them and inform you in writing.

- If, as per your instruction the recovered amount is paid directly to Direct Redress Limited, we will deduct our agreed fee and forward the rest of the amount awarded.

to you without delay. If the payment is made directly to you, which can happen on occasion, we will forward an invoice to you for payment.

- If your claim is successful, we must advise that your Payment Protection Insurance may be cancelled.

- What is it that Direct Redress Limited will not do for you?

- We will not offer or give you financial advice.

- We cannot guarantee to win a claim we accept and pursue.

- We will not take your case to court (we will however inform you if we think that you should).

- What is it that we require you to do?

- We ask that you provide all relevant information we may request without delay, this will enable us to pursue your claim efficiently.

- Co-operate fully with us

- Not to mislead us or ask us to act in an improper or unreasonable way.

- To provide us with the authority for the duration of the contract;

(a) to pursue your claim,

(b) to enter into correspondence and negotiations on your behalf,

(c) to receive, process and provide valid receipt for any remuneration made,

(d) to ask the financier of the cheque (for your compensation payment) to make it payable to Direct Redress Limited so that we can process it, deduct our fee, as set out in this Agreement, before forwarding the balance to you.

- If payment is made directly to you, you must pay our invoice within 14 days.

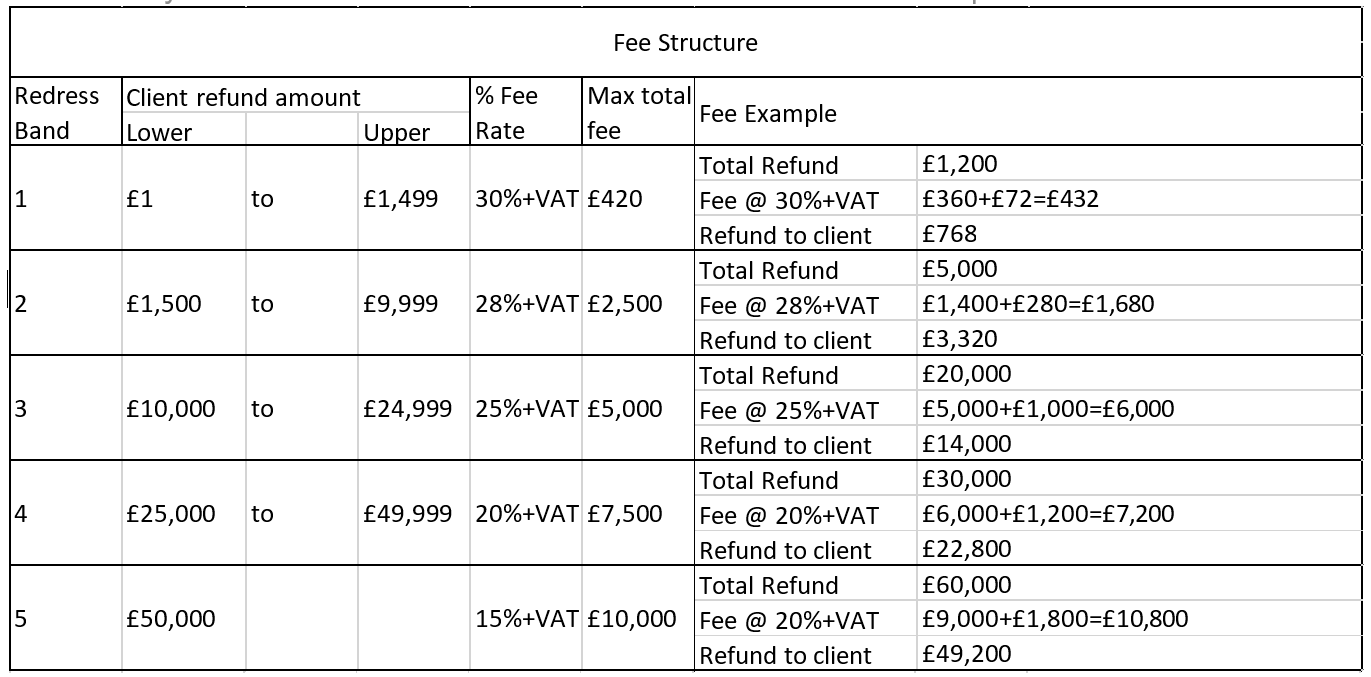

- Our Fees

- In the unlikely event that we do not succeed in obtaining compensation, you pay us nothing.

- Our fees are charged in accordance with FCA guidelines, calculated from the total value of all compensation which is awarded to you for each claim. We have set out the fee bands and examples of our fees below:

- We have set out 3 examples of how compensation and our fee may be paid:

| How you are compensated | Total Offer Awarded | Funds you receive | Our Fee to be paid |

| Cash in hand only | £3,000.00 cash | £3000.00 | £1008.00 (£840 + £168 VAT) |

| £2,000.00 cash | £2000.00 | £672.00 (£560 + £112 VAT) |

|

| £1,000.00 cash | £1000.00 | £360.00 (£300 + £60 VAT) |

|

| Part cash and part offset against arrears or existing borrowing | £2,000.00 cash £1,000.00 offset |

£2000.00 (£3000 – £1000 offset) |

£1008.00 (£840 + £168 VAT) |

| £1,000.00 cash £1,000.00 offset |

£1000.00 (£2000 – £1000 offset) |

£672.00 (£560 + £112 VAT) |

|

| £500.00 cash £500.00 offset |

£500.00 (£1000 – £500 offset) |

£360.00 (£300 + £60 VAT) |

|

| Fully used to offset arrears with the Bank | £3,000.00 offset amount | £0.00 (£3000 offset amount) |

£1008.00 (£840 + £168 VAT) |

| £2,000.00 offset amount | £0.00 (£2000 offset amount) |

£672.00 (£560 + £112 VAT) |

|

| £1,000.00 offset amount | £0.00 (£1000 offset amount) |

£360.00 (£300 + £60 VAT) |

Non Payment of Invoice (Cash in hand)

Without exception, all invoices must be paid in full upon completion of your case by the lender. The costs of any telephone calls and invoice reminders may be added to the outstanding debt :-

£10+VAT second and subsequent written reminder

£25+VAT second and subsequent telephone reminder

£50+VAT Solicitors Letter Before Action

Non Payment of Invoice (Offset to Arrears/Outstanding Balance)

Without exception, all invoices must be paid in full upon completion of your case by the lender. The costs of any telephone calls and invoice reminders may be added to the outstanding debt :-

£10+VAT second and subsequent written reminder

£25+VAT second and subsequent telephone reminder

£50+VAT Solicitors Letter before Action

Debt Recovery

The cost of any County Court action will be added to the outstanding debt together with statutory interest, pursuant to Section 69 of County Court Act 1984 until the debt is paid in full.

- How Direct Redress Limited will collect our fees

You are responsible for the payment of our fees within 14 consecutive days of the invoice being issued. These fees must be paid from the amount you are awarded.

PPI (Loan or Credit Card)

(a) If your loan has been paid off in full you will receive your award in the form of a cheque or bank transfer for the full amount of the refund, including interest that has been incurred, and interest at 8% on the money recovered. However, if the loan was/is in arrears, it is likely the compensation would be used to primarily off-set those arrears.

Once we have been made aware that you have received your settlement (either via notification from you or the Third Party) our agreed fees will be payable.

(b) If your loan is still in force (e.g. you are still paying the loan)

Your settlement may come in 2 parts

(Part 1) You will be refunded either the commission or the Premiums you have paid into your policy to date, along with the interest that you have incurred and further interest of 8% on this amount.

(Part 2) In addition, the Premiums you are still scheduled to pay during the remainder of your loan may be removed from your loan and your monthly repayments therefore reduced as a result of this.

If this is the settlement that you receive, our fees will be calculated from a combination of the amount recovered in a cash sum and the amount we have reduced your loan by. We expect our fees to be paid out of the lump sum you receive. If you benefit financially by way of a reduction of an existing debt (such as arrears); Direct Redress Limited require our fees settling on this matter, as set out in Clause 4 of the Terms of Engagement.

Credit Card Charges

- The credit card company pays the settlement directly to you or if they reduce any of your credit balances by the settlement amount, then you will be liable to pay the fee (and any additional costs paid on your behalf) direct to Direct Redress Limited.

- a) You agree to notify Direct Redress Limited of any settlement received from the Credit Card company within 3 days of receipt.

- b) We will issue an invoice for our services which will be payable immediately.

Packaged Bank Account

- If the Lender pays the settlement directly to you or if they reduce any of your balances by the settlement amount, then you will be liable to pay the fee (and any additional costs paid on your behalf) direct to Direct Redress Limited.

- a) You agree to notify Direct Redress Limited of any settlement received from the Lender within 3 days of receipt.

- b) We will issue an invoice for our services which will be payable immediately.

Undisclosed Commission

If your complaint is affected by undisclosed commission, our fees would be payable in

accordance with Section 4.

Irresponsible/Unaffordable Lending

If your complaint is affected by irresponsible or unaffordable lending, our fees would be payable in

accordance with Section 4.

- Cancellation of this Agreement

- We reserve the right to cancel this Agreement at any time. There will be no fee payable if we advise you that your claim is unlikely to succeed and you have fulfilled your obligations (as laid out in section 3 of this agreement).

- There will be no fees payable if you cancel within 14 days of this agreement.

- If this agreement is cancelled (by either party) when an offer of payment has been made, we will enforce our charges, plus any fees which may have been incurred by us in the administration of your claim.

- If you cancel this Agreement prior to any offer or settlement has been made, we reserve the right to charge you reasonable costs for the administration of your claim, up to the point at which you informed us you would like to cancel.

- Cancellation of this Agreement by either party must be in writing, delivered by recorded delivery post, or by email.

- The Complaints Procedure

The Company operates a complaints procedure, full details of which are available upon request.

- Data Protection

- Information and documentation you provide to us to enable us to perform the Services may constitute personal data under the Data Protection Act 2018 and UK GDPR. We will comply with the law as applicable.

- We may pass your personal data to the lender and/or the Financial Ombudsman Service to perform the Services or to the extent we are legally obliged to do so.

- We refer you to our Privacy Policyon the Website, in which we set out how we process your personal data, and how you may contact us regarding our processing.